Most People Will Never Invest. Not Because They Can't.

The two mental blocks stopping you from the greatest wealth-building tool available to ordinary people - and how to get past them.

Charlie Chan

April 07, 2026

Wisdoms from Chamath Palihapitiya

Most people will never seriously invest.

Not because they can't afford to. Not because the stock market is too complicated. Not because they don't have time.

Because they've convinced themselves of one of two things: "I don't have enough money to make it worth it" or "I'll probably just lose it."

I've been thinking about this a lot after watching Chamath Palihapitiya - early Facebook exec, Social Capital founder, billionaire investor - break down his core investing philosophy. The man has torched $5 billion in a single year (his words, not mine), bought 10% of the Golden State Warriors for $25M and watched it grow to $900M, and spent decades studying what separates people who build real wealth from people who don't.

His answer isn't what you'd expect from a billionaire. It's not stock picks. It's not secret strategies. It's two mental unlocks that most people never make.

Why Investing Is the Best Opportunity You're Not Taking

Here's something worth sitting with: your salary grows at roughly 3-4% per year on average. The S&P 500 has returned roughly 10% per year over the last 20 years.

That gap is everything.

If you only grow your income, you're limited to your own output - your hours, your skills, your employer's goodwill. But when you invest, you're buying a stake in other people's intelligence, work, and innovation. Apple's engineers. Microsoft's cloud infrastructure. Nvidia's chip design. You don't need to understand any of it. You just need to own a piece of it.

This is the fundamental insight most people miss. Investing isn't gambling on price movements. It's buying a seat on humanity's compounding progress. Your salary is one stream of income, tied entirely to you. Investing lets you tap into thousands of streams at once.

The only catch? You have to actually start.

Mental Block #1: "I Don't Have Enough Money"

This is the most common objection, and it's the most wrong.

Chamath's illustration makes this concrete. He sat with a famous athlete who'd just signed a massive contract - think tens of millions. He built them a compound interest table: take the salary, subtract taxes, agents, managers, what's left. Watch it compound at 8-10% for 30 years. Mind blown.

Then he did it again with 1/1000th of that number.

Mind still blown.

That's the power of compounding. The starting amount matters far less than you think. What matters is time and consistency.

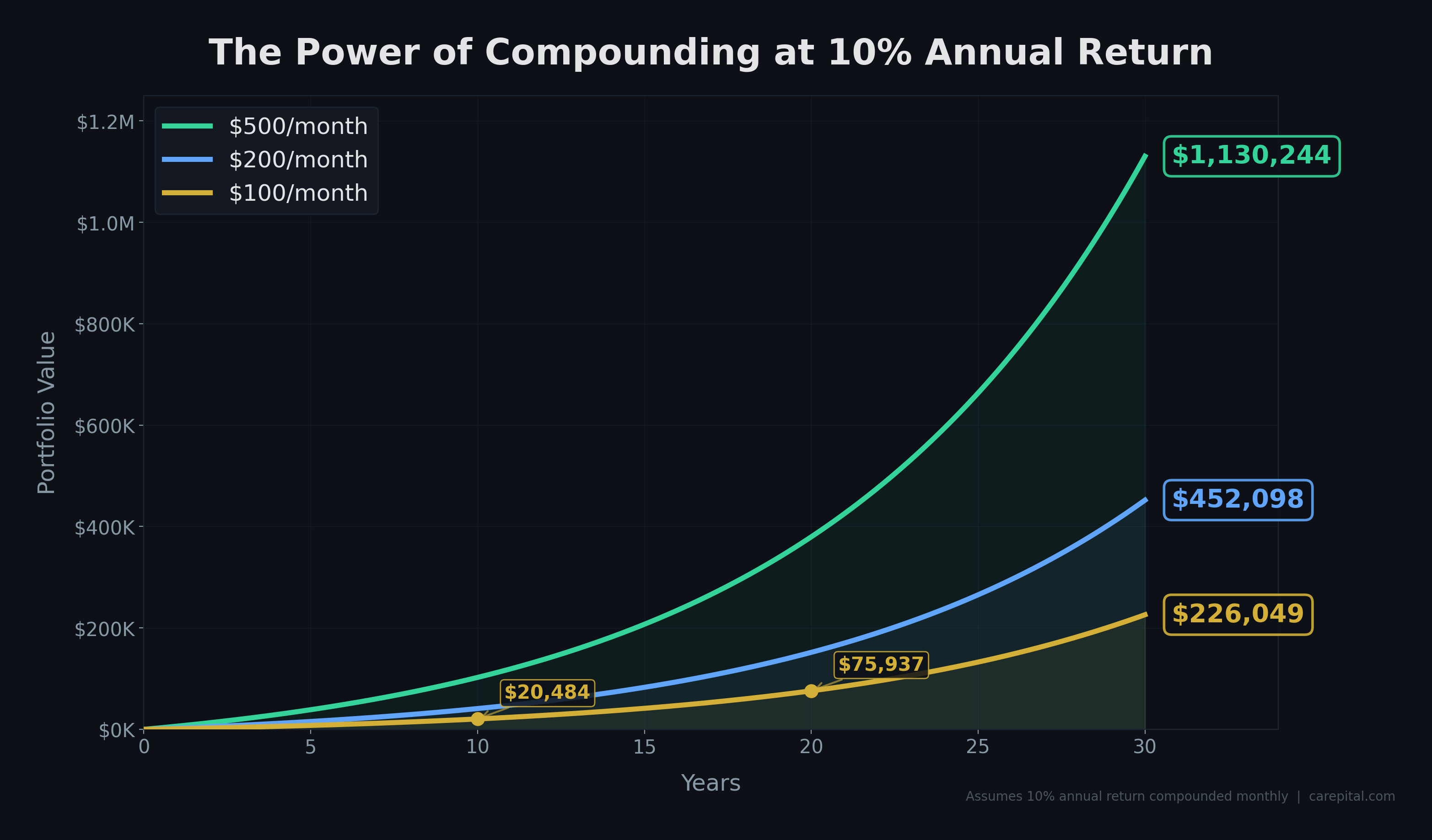

Here's the math for a normal person:

Monthly Investment | Years | Total Contributed | Value at 10%/year |

|---|---|---|---|

$100 | 10 | $12,000 | ~$20,000 |

$100 | 20 | $24,000 | ~$76,000 |

$100 | 30 | $36,000 | ~$227,000 |

$200 | 30 | $72,000 | ~$453,000 |

$500 | 30 | $180,000 | ~$1,130,000 |

$100 a month for 20 years. That's $3.30 a day. The total you put in is $24,000. What you end up with: around $76,000 - over three times your investment, compounded on autopilot.

Nobody is going to tell you this with any urgency because there's no commission in it for them.

The people who mock small starting amounts - "what's the point of $50?" - are doing so because it makes them feel better about their own decisions to do nothing. Don't let someone else's insecurity become your financial inaction.

Chamath puts it bluntly: "Just start and don't tell anybody. Show up 10-15 years later with a huge war chest."

Mental Block #2: "I'll Lose Money"

Yes. You probably will, at some point. So will everyone else.

Chamath lost roughly $5 billion in 2021-2022. Here's what happened: In November 2021, he watched Jeff Bezos and Elon Musk start selling their own company stock. Two of the best capital allocators on earth were quietly reducing exposure. He knew what it meant. He sold a little. Not nearly enough.

Why? Because he'd confused his growing fame with growing skill. He was afraid of what people would think if he told his followers to sell. So he held. Then Russia invaded Ukraine in March 2022, interest rates spiked, and his SPAC positions got obliterated. $5 billion, gone.

The lesson he took from it: "When the people structurally smarter than you do things against the grain of what you've done, immediately do the same thing. Then prove to yourself why you shouldn't."

But here's the part almost nobody talks about when it comes to investing losses in the US: your losses carry forward indefinitely.

If you lose $1,000 in the market, you get a $1,000 capital loss that you can use to offset future gains - with no expiration date. So when you eventually make $1,000 in profit, you owe zero tax on it.

Losses aren't a dead end. They're a deduction you can use for the rest of your investing life.

This doesn't mean losses don't hurt. They do. But they're not the catastrophic, permanent damage your brain imagines when you think "what if I invest and lose it all?" The tax system is actually built to let you recover and course-correct.

What you do have to own is the decision. Chamath is clear on this: if you can't take complete responsibility for every position you hold, don't be in individual stocks. Put it in an index fund and move on. That's not a cop-out - that's actually smart risk management.

The Barbell: How to Structure Your Risk

Once you've started, there's a framework worth borrowing from how Chamath thinks about his own portfolio.

He calls it the barbell.

On one end: concentrated, high-conviction bets - for him, technology companies with asymmetric upside. On the other end: an uncorrelated hedge that effectively acts as cash.

The Warriors investment is the famous example. He bought 10% of the Golden State Warriors for $25 million in the mid-2000s. His reasoning had nothing to do with basketball. He needed something uncorrelated to tech - something that would hold value even if all his tech bets went to zero. Sports franchises fit. Today, that 10% stake is worth $700-900 million. He sold some of it for $500 million.

But the more important point: that hedge gave him the mental freedom to take concentrated tech risks. Without it, every market downturn would have felt existential. With it, he knew he had a floor.

You don't need a sports franchise. But the principle applies at any scale:

Put most of your portfolio in things you understand and believe in (index funds if you're starting out, individual companies once you've built conviction)

Keep a portion in something genuinely uncorrelated - cash, bonds, real estate, or whatever you can sleep through a 30% drawdown with

The barbell isn't just a financial structure. It's a psychological one. It's what allows you to hold your positions without panic-selling at the worst moment.

How to Actually Start

Chamath's framework for where to begin is disarmingly simple: look at the products you love.

His younger son, at 8 years old, bought Xbox, PlayStation, and Nintendo after getting $100 from a golf bet. Steady compounder. 30% annualised return over 3 years.

His older son bought Virgin Galactic on price action, turned $200 into $3,000, bought a computer, and never touched the stock market again.

Same starting point. Different approach. One bought things he understood and used every day. One chased price action on a story he heard.

The lesson: "Look at the products you love, that are well-made, that you would pay for happily. Find out who makes them."

That's a real strategy. If you love a product enough to pay for it happily, and the company behind it is public, there's a reasonable chance others feel the same way. That's not naive - that's how Peter Lynch built one of the best track records in fund management history.

Practical first steps:

Open a brokerage account this week.

Set up automatic monthly contributions - even $50 or $100.

Start with a broad index fund (VTI or VOO) if you don't have conviction in individual stocks yet

Build your compound interest table. Seriously. Do it in a spreadsheet. Watching those numbers over 20-30 years will change your relationship with short-term noise.

Don't tell anyone you've started. Just do it.

My Take

Here's what I keep coming back to: most people don't invest because the downside feels vivid and the upside feels abstract.

Losing $500 is concrete. It happened. It hurt. "Having $76,000 in 20 years from $100/month" is a spreadsheet projection that doesn't feel real.

But that gap between vivid downside and abstract upside is exactly what Chamath's two rules address. The compound interest table makes the upside tangible. Understanding tax-loss carryforwards shrinks the downside to something manageable.

The real cost of not investing isn't the money you might lose. It's being permanently limited to your own output in a world where capital compounds automatically for everyone who shows up.

You don't need to be a genius. You don't need special access. You need to start early, stay consistent, and not do anything catastrophically stupid.

That's the whole game. It's boring. It works. Start.

I write about investing, markets, and building wealth for people who are thinking seriously about their financial future. If this was useful, forward it to someone who's been "meaning to start investing" for the last three years.

Enjoyed this issue?

Subscribe to get new insights delivered to your inbox.

Join the newsletter

An investor's notebook. The research, the conviction, and the bets behind every position.

No spam. Unsubscribe anytime.